As Australia’s mortgage market continues to evolve, recent developments highlight an increasingly competitive environment for borrowers seeking fixed-rate home loans. In a noteworthy move, NAB (National Australia Bank) recently adjusted its three-year fixed-rate home loan to 5.99%. Now, Macquarie Bank has followed suit, reducing its two-year fixed rate to a highly competitive 5.79%. These changes are significant, particularly in the context of the current cash rate trends set by the Reserve Bank of Australia (RBA).

The Competitive Edge in Fixed-Rate Home Loans

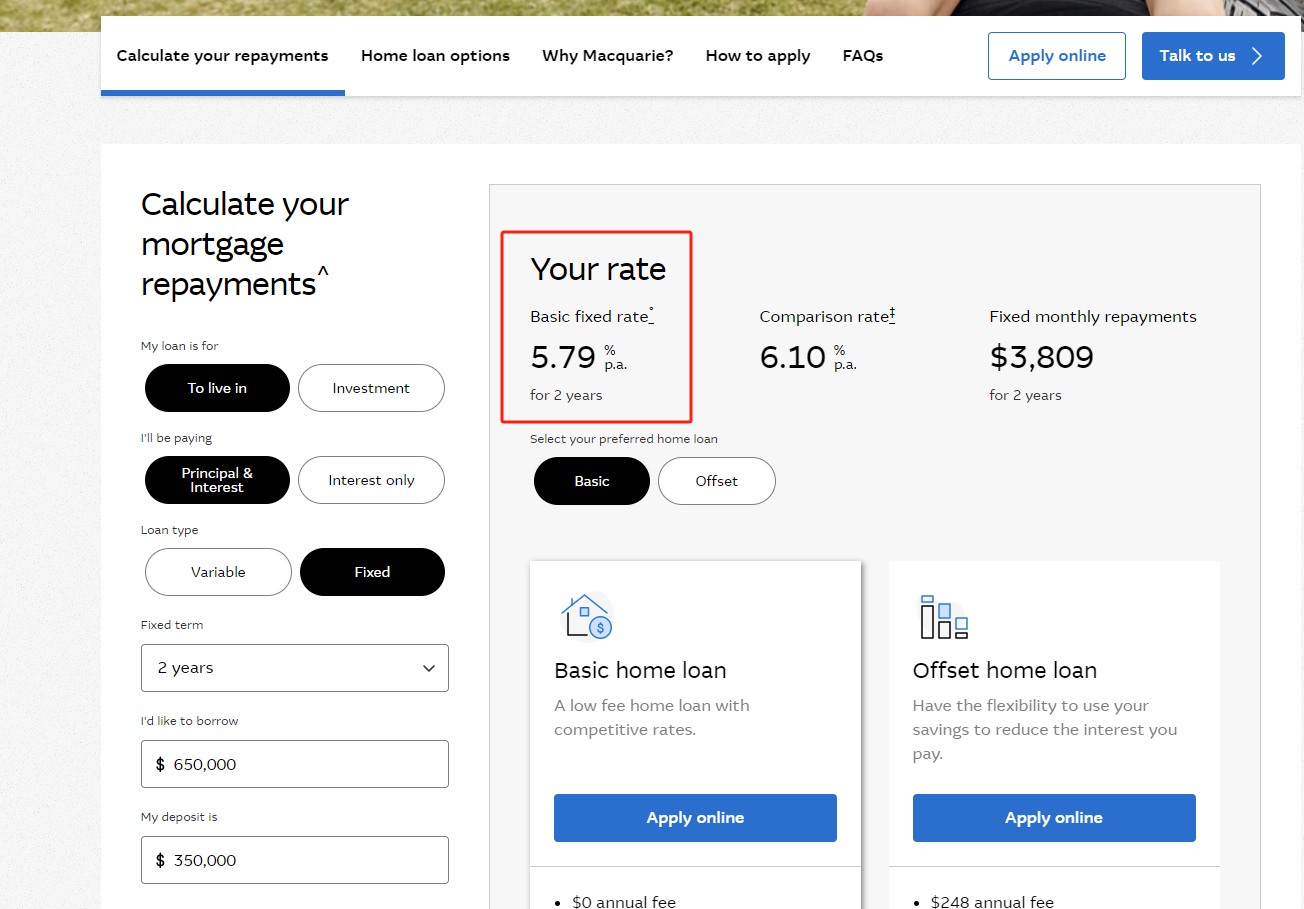

The reduction in fixed rates by major players like NAB and Macquarie Bank indicates a strategic shift in the lending market. Fixed-rate loans are often preferred by borrowers looking for stability in their mortgage repayments, particularly in an uncertain economic climate. The 5.79% rate offered by Macquarie Bank is especially appealing, as it undercuts many of its competitors and provides a level of certainty for borrowers over a two-year period.

For borrowers, the appeal of these rates lies in their ability to lock in relatively low repayments for a fixed period, shielding them from potential future increases in variable rates. Given the backdrop of a fluctuating cash rate environment, this predictability can be crucial in managing household budgets.

The RBA’s Cash Rate and Its Implications

The RBA’s cash rate decisions are the primary driver behind the movements in mortgage rates across the country. As of recent months, the cash rate has been a focal point for both borrowers and lenders, with adjustments made in response to inflationary pressures and economic performance. The RBA has been cautious, balancing the need to curb inflation while also ensuring that economic growth is not stifled.

While the RBA has made several increases to the cash rate to address rising inflation, there have been signs that these hikes might be slowing. This potential stabilization of the cash rate provides a window of opportunity for lenders to offer more competitive fixed rates, as the immediate threat of significant rate hikes diminishes.

What This Means for Borrowers

For current and prospective homeowners, these competitive fixed-rate offerings could be a timely opportunity. Locking in a rate of 5.79% with Macquarie Bank for two years could be particularly beneficial if the cash rate remains stable or increases slightly in the near term. Borrowers should carefully consider their financial situation, future interest rate expectations, and personal preferences when choosing between fixed and variable rate loans.

Additionally, with multiple lenders adjusting their fixed rates, it may be wise for borrowers to shop around and compare options. The current market dynamics suggest that there may be further rate adjustments on the horizon, especially if competition among lenders intensifies.

Conclusion

The recent moves by NAB and Macquarie Bank underscore a shifting landscape in Australia’s mortgage market. With the RBA’s cash rate playing a crucial role in determining lending rates, the introduction of competitive fixed-rate loans provides borrowers with options to navigate potential economic uncertainties. As always, it’s essential for borrowers to stay informed and consider both current offers and long-term financial implications when choosing a mortgage product.

Looking to purchase an investment property? All Seasons. Finance is here to assist you every step of the way. To explore your options, please contact us at 02 8041 6528, email us at info@allseasonsgroup.com.au, or fill out our online form.